The headline was jarring: “Brace yourself – inflation is coming back stronger than ever”. The Consumer Price Index in July stood at 5.4 percent over a year ago and the Producer Price Index was up 7.8 percent. The writer concluded the “financial chickens have finally come home to roost” and the United States is headed toward a “new inflation-dominated” era.

Charts published by The New York Times showing annual price fluctuations from 50 product categories painted a less alarming picture. They show declining prices for 27 categories, including prescription drugs, men’s suits, infant apparel, cosmetics, computer software, processed fruit and health insurance.

“So far, the inflationary burst of 2021 has been overwhelmingly driven by a narrow group of sectors that were deeply affected by the shock of COVID-19 and last year’s accompanying shutdowns,” according to Josh Bivens, director of research at the nonprofit Economic Policy Institute, and Stuart Thompson who writes for Opinion, who urge patience in combatting inflation.

As an example of what Federal Reserve Chair Jerome Powell describes as “transitory” inflation, Bivens and Thompson cited used cars, which experienced steep price increases earlier in the pandemic, but saw significant price deceleration in July.

Alvaro Vargas Llosa, a political commentator and opinion contributor to The Hill, wrote, “The Federal Reserve insists that the current price inflation is transitory. However, every sign points in the opposite direction and we need to understand the economic and political implications of what is about to begin – an era of high inflation.”

“A country cannot raise its debt by 40 percent in two years (as the federal government has done since 2019, according to my calculations) or spend more than $6 trillion in 2020, incurring a 15 percent fiscal deficit on top of years of prior profligacy, without consequences,” Llosa says. “Nor can the Fed spend money to buy assets, increasing its balance sheet to more than $8 trillion (up from $4.3 trillion in 2019) and not expect that money to spill out into the economy at some point. There are signs that this is already happening – and it is only the beginning.”

Bivens and Thompson insist price increases are a sign of economic growth, not impending financial doom. “It may surprise Americans that even during times of strong economic growth and very low inflation…more than half of all goods and services are usually experiencing price increases.” The same is true, they add, for periods of weak growth and low inflation.

The current spate of price increases in some sectors can be explained, Bivens and Thompson contend, by the V-shaped economic recovery. “The near-collapse and rapid bounce-back of several coronavirus-affected sectors, such as travel, led to what economists call ‘base effect’ – when the year-over-year price increases are sharp, but only because they’re coming back from a low point caused by economic shock.”

It may surprise Americans that even during times of strong economic growth and very low inflation…more than half of all goods and services are usually experiencing price increases.

Llosa also warns of stockpiling federal government financial obligations as more older adults qualify for Social Security and Medicare and pressures to turn away from the US dollar as the world’s reserve currency. “There is simply no way for the US government to pay what it owes, but it can inflate its way out of a big chunk of that debt,” Llosa says.

Bivens and Thompson make a warning in the opposite direction. Asking the Fed to cool off the economy through higher interest rates, they claim, would risk stalling the nascent economic recovery. “Cheaper furniture, fast food, used cars and airfares would be nice,” they say, “but they aren’t worth cutting the economic recovery short.”

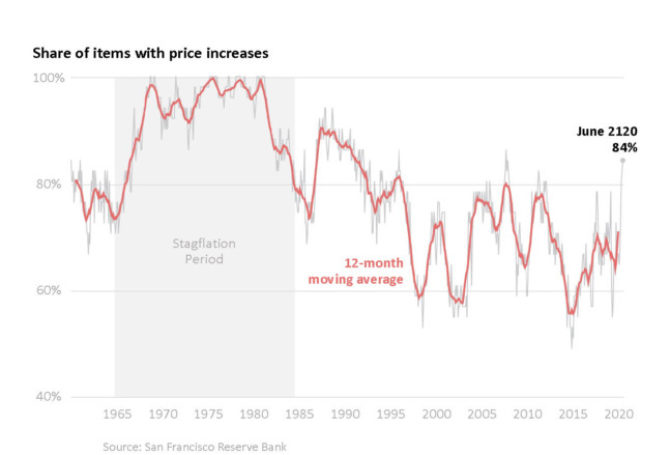

The data Bivens and Thompson rely on comes from the San Francisco Federal Reserve Bank, which monitors economic sectors for price increases. “So far in 2021, [price increases] don’t look much different from the previous year, signaling that unusually high inflation seems contained in a subset of sectors. It bears no resemblance to the 1970s when the combination of slow economic growth and high inflation led to the phenomenon called ‘stagflation’.”

They anticipate sectors experiencing significant price increases will begin to taper off as consumer demand wanes. “Once sectoral balance is restored,” Bivens and Thompson say, “inflation will quickly normalize – without any need to rein in macroeconomic stimulus.”