His Challenge: Explain Why More Jobs Equate to Good Economic News

President Biden gives his second State of the Union address tonight with the challenge of explaining strong job growth and historically low unemployment in the face of prevalent opinion the economy is a mess, as well as a critical House GOP majority.

Polling shows many Americans view inflated prices as a continuing problem. An even larger majority blames government as Biden and House Republicans are in a stare-down over raising the national debt ceiling.

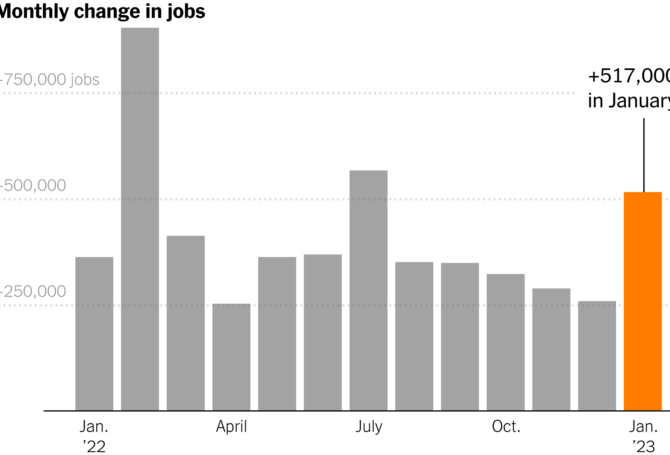

The backdrop for the speech is U.S. hiring that unexpectedly rose by 517,000 jobs in January, dropping the national unemployment rate to 3.4 percent, its lowest level in 50 years. Capital markets reacted negatively, fearing all those new workers could fan inflation. Some experts called robust hiring in January a seasonal quirk.

President Biden delivering his first State of the Union address a year ago to a Democratically controlled Congress.

As a rule, growing employment is seen as good economic news. So why did all those new hires in January turn smiles into frowns? Market watchers believe an overheated labor market could persuade the Federal Reserve to keep raising interest rates and retain those high rates longer.

“A stunningly strong jobs report raises serious doubts about the economy slipping into recession and the Fed ending its tightening cycle this spring,” insisted Sal Guatieri, senior economist at BMO Capital Markets.

The good news-bad news scenario is more puzzling because data shows there are still 11 million unfilled jobs in the United States, even after 1,000 technology companies laid off 152,000 workers last year and announced 66,000 layoffs so far this year.

The Bureau of Labor Statistics (BLS) reported the national unemployment rate inched down to 3.4 percent, with 5.7 million unemployed workers and 2.1 million unemployment insurance claims. Unemployment for Black workers also reached a historic low of 5.4 percent. The U.S. unemployment rate hit a high of 14.7 percent in April 2020 during the peak of the pandemic. Between 1948 and 2023, the average national unemployment rate has been 5.73 percent.

BLS provided additional insight into the job market. In December, there were 6.2 million hires and 5.9 million “separations” that including quits (4.1 million) and layoffs (1.5 million). The largest increases in job openings were in food and hospitality (409,000), retail (134,000) and construction (82,000). Job openings in December increased in small and medium-sized employers and decreased in employers with 5,000 or more workers. Its next report will come out March 8.

The U.S. Labor Department reported the annual inflation rate in December stood at 6.5 percent, down from 7.1 percent in November, 7.7 percent in October and 9.1 percent earlier last year. Before the latest jobs report came out, the Fed responded to declining inflation rates by approving only a quarter point interest rate hike.

BLS pegged wage growth in 2022 at 5.1 percent. Compensation in 2023 is expected to average 3.8 percent, though some economists predict it could increase by up to 5 percent as employers continue to struggle to hire and retain workers.

The addition of new jobs and wage growth helped to propel a January bounce-back in consumer spending. The U.S. Census Bureau reported a 3.8 percent increase over December. Non-store sales (including online sales) rose 14.5 percent, department stores 9.2 percent and furniture 7.2 percent.

The data make it hard to describe an economy in shambles or teetering on the brink of recession. The explanation could as simple as this is the picture of the economic soft-landing Fed Chair Jerome Powell is trying to engineer. The plane may be coming in hot, but it isn’t in any apparent danger of crashing.

The last soft landing engineered by the Fed occurred in 1994 following a brief recession sparked by spiking oil prices after Iraq invaded Kuwait. Even though the inflation rate was only 3 percent, the Fed doubled interest rates to 6 percent to stabilize prices. The inflation rate remained at 3 percent before drifting down while unemployment continued to decline. Alan Blinder, a Princeton economics professor who was vice chair of the Federal Reserve’s Board of Governors then, credits the successful soft landing to “luck and skill.” He said the “luck” involved the absence of “serious supply shocks” and the skill was acting “preemptively”.

Economic fortunes often depend on what economists call externalities – unexpected events that create chaos like a war, supply chain disruptions, major weather event, earthquake or capital market meltdown. The Russian invasion of Ukraine, which caused considerable disruption in global energy and grain markets, has not apparently had a sustained inflationary impact on the U.S. economy. Chinese-related supply disruptions have abated and the computer chip shortage has turned into a glut. The price of gas at the pump has dropped markedly, despite weekly blips.

Current global inflation is rooted in the impact of the COVID pandemic that led to massive business shutdowns. As businesses re-opened and national economies began to rebound, consumer demand and supply were misaligned. Aggressive fiscal policies put money in consumer pocketbooks before manufacturers and their supply chains could deliver the products they wanted to buy.

The challenge facing policymakers was to avoid letting the world slip into recession by pumping lots of money into the economy and risking a spike in inflation. The challenge facing the Fed, which has the only real inflation-fighting tool in setting interest rates, was not acting too soon to avoid slowing down business recovery and exacerbating supply shortages.

While it’s easy to find fault in hindsight with decisions made and not made by policymakers in control of fiscal and monetary policy, the current economic conundrum is more or less predictable – and the lesser of two evils. It’s possible fiscal stimulus was too great and monetary policy was too tardy, but U.S. economy heading into 2023 on a strong note with growing employment and declining unemployment isn’t so bad – and a whole lot better than many of the alternatives.

Many of the problem areas we see, such as job layoffs in the tech sector, may not be centered on inflation, but reflect overzealous hiring and changing market conditions. The tech sector layoffs also may presage new directions, including pursuit of artificial intelligence and virtual reality technologies.

Lost in the shadow of headlines about inflation is the resurgence of small business.

Lost in the shadow of headlines about inflation is the resurgence of small business. Many of the entrepreneurs saw the pandemic as a unique opportunity to break ties to a corporate workplace and follow their dream. Data indicates small businesses account for nearly two-thirds of new job creation and 44 percent of overall U.S. economic activity.

In his speech, Biden will defend his economic policies, continuing support for Ukraine and new immigration policies to lessen pressure on the southern border. There may not be enough time for him to explain why 500,000 new jobs is a good thing.